The “War Tax” on Energy: Geopolitical Spillovers in 2026

In March 2026 a sudden escalation in the Middle East (U.S.-Israeli strikes on Iran and Iranian reprisals) caused a sharp jump in oil and gas prices, the so-called “war tax.” Brent crude shot up nearly 5% on March 5, and spot European gas spiked ~20% as tanker traffic in the Strait of Hormuz was disrupted. Insurance premiums and shipping costs soared: over 150 ships anchored in the Gulf, war-risk coverage was cancelled for Hormuz voyages, and spot tanker rates (TD3C) almost tripled to $12 million per voyage. OPEC members (Iraq, Qatar) and others suspended production when ships could not export. These disruptions are now being passed through to consumers worldwide. In Europe, surging Brent and gas prices raise fuel and heating costs and threaten inflation – ECB staff estimate gas was already ~€30/MWh but winter surcharges may rise. In India, the Finance Minister noted that a 10% crude increase adds ~0.3 percentage point to inflation (the Indian basket jumped from $69 to $80 in days). In China and Asia, imports (via the Gulf or rerouted routes) became more expensive, incentivizing Beijing’s emphasis on industrial “self-reliance.” China’s 2026 budget (released Mar 6) reinforces high-tech and manufacturing (semiconductors, renewables) to shield against such shocks.

Energy supply fear is compounded by chokepoint risk: roughly 20% of global oil (and large LNG volumes) transit Hormuz. With the Strait closed and Gulf exports halted, some tankers now sail via the Cape of Good Hope, lengthening voyages by weeks. The EU and other consumers are using policy tools: several countries released strategic petroleum reserves, and the EU’s Anti-Coercion Instrument (ACI) was invoked to protect member economies (notably Spain’s trade with Iran). Possible scenarios include a protracted lull in Gulf exports (causing sustained inflation and demand destruction) or a quick diplomatic resolution leading to partial normalization. Policy options range from releasing reserves and subsidizing insurance to aggressive diplomacy. A summary timeline and policy flowchart are provided below. Key recommendations: stockpile releases and LNG diversions should be coordinated internationally; Europe must bolster demand resilience (e.g. energy efficiency); insurers and navies should secure alternative routes; and diplomatic channels (EU regional dialogues, China multilateralism) should de-escalate pressures to prevent “war tax” spillovers from becoming entrenched inflation.

Middle East Escalation and Immediate Market Impacts

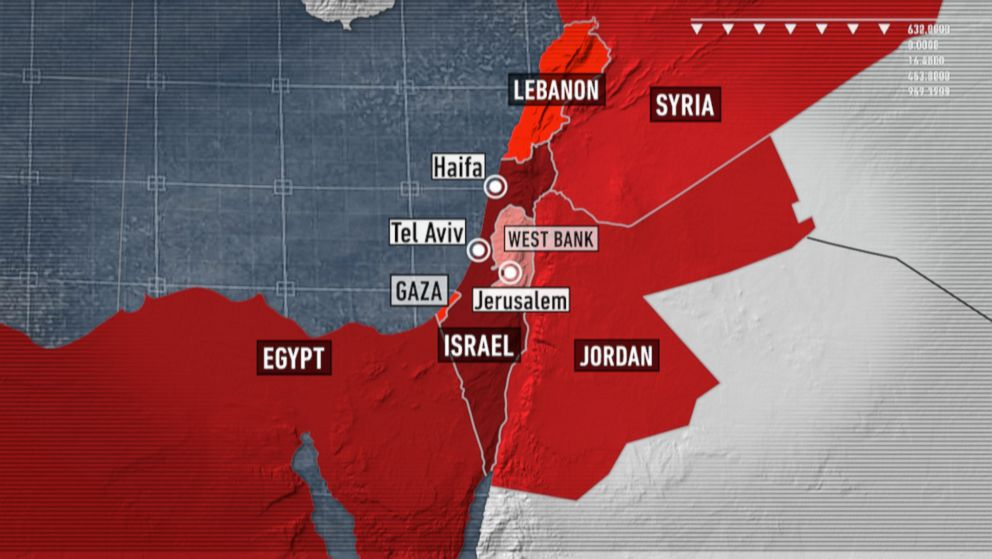

On 28 February 2026, Israel and the U.S. launched air strikes on Iranian territory (retaliation for prior attacks), prompting Iran to respond with missile strikes and naval harassment. By 1–2 March, Gulf shipping was paralysed. Over 150 vessels (oil tankers and LPG carriers) anchored in the Gulf as a precaution. War-risk insurers cancelled coverage effective March 5. Key routes were closed: Iran declared the Strait of Hormuz blocked, and major carriers (Maersk, Hapag-Lloyd, CMA CGM) rerouted ships around the Cape of Good Hope. Hapag-Lloyd imposed surcharges for Gulf cargoes, reflecting sharply higher risk.

The price reaction was immediate. U.S. crude (WTI) jumped ~8.5% (to $81.01) and Brent ~4.9% ($85.41) on March 5. On March 2 alone Brent had been up ~8% and Dutch gas +19%. Analysts note that about one-fifth of global oil flows through Hormuz, so any disruption tightens supply. Middle Eastern OPEC producers (Iraq, Qatar) cut output because they could not get tankers out. Chinese fuel exports were also curtailed. Oil inventories in the region are limited, so the loss of supply is felt in real-time. Refineries in the Middle East, China and India temporarily shut units due to crude shortages.

Shipping costs skyrocketed too. Benchmark freight (TD3C) for VLCCs Middle East-to-Asia tripled since early 2026, reaching ~$12 million per voyage. As one broker notes, rates were rising “exponentially”. Ships that could not cross Hormuz or Suez (due to concurrent Red Sea issues) began long detours around Africa. This surge in transit cost adds to energy prices: the additional days at sea translate to millions more per cargo, likely feeding into higher fuel prices globally.

Insurance premiums followed suit. Major P&I clubs cancelled war-risk cover for Hormuz and adjacent waters. Some underwriters began offering cover only on a special “buyback” basis. War risk premiums surged to prohibitive levels (reports indicated premiums for Gulf voyages became effectively unusable). In practice, governments have considered subsidizing insurance or providing sovereign-backed guarantees to ensure at least some trade flows continue.

Pass-Through to Consumer Prices

The spike in energy prices is now filtering into consumer markets. Global oil prices rose ~20-25% in days, so one expects higher fuel and heating costs. The degree of pass-through varies by region:

Europe: As Reuters notes, Europe depends on Gulf oil, LNG and propane (20% global oil via Hormuz). German pump prices climbed 8-10% immediately. With EU gas prices jumping ~19%, electricity and heating bills will rise. Historically, roughly half of a crude oil price rise can show up in gasoline prices within 2-3 months. Inflation models from the ECB suggest even an 8% oil jump could add ~0.2-0.3 percentage points to euro-area inflation. The ECB had assumed $62.5/barrel in projections; at $78 now, energy inflation forecasts will be revised up. However, many European governments maintain buffer policies: for example, France and Spain have fuel tax rebates and VAT cuts. Britain has already capped household energy bills this winter, so their pass-through to consumers is partly limited. Analysts think the net effect may be a 0.5–1.0% boost in headline CPI for Europe over 6–12 months, unless offset by fiscal measures.

Middle East & North Africa (MENA): Oil producers in the Gulf generally have low domestic prices (fuel heavily subsidized). Thus, local pump prices in Iran, Iraq, UAE, etc., may barely budge. In Iran itself, economic turmoil and sanctions complicate pricing, but petrol remains heavily controlled. In resource-poor MENA (e.g. Egypt, Tunisia), higher imported fuel costs will affect inflation more. Many countries (Egypt, Jordan) have liberalized fuel prices, so their CPI could rise by a few tenths. However, these states often have larger inflation buffers (subsidy caps, stockpiles). Overall, pass-through in producers will be minimal to none; in importers, moderate but not extreme.

Asia (India, China, Japan, etc.): Asia is a major oil importer. India’s finance minister expects only a modest inflation impact: the RBI estimates a 10% oil increase adds ~0.3 pp to inflation. India’s retail inflation was ~2.8% in Jan 2026, so the recent 20-25% oil jump could lift inflation by ~0.5 0.8 pp if fully passed on. In practice, India has partly absorbed cost via tax cuts on petrol and diesel. China’s CPI is running low (0–1%); it too has tools like strategic reserves and price controls for refined fuels. East Asian economies (Japan, S Korea) import most oil, but often have stable tax schemes, so again a fraction of the price rise passes to consumers. In sum, Asia’s inflation hit will likely be contained under 1 percentage point due to policy buffers (subsidies, tax cuts).

In all regions, heating fuel (LNG, propane) and transport (jet fuel) are also affected. Europe imports LNG via pipelines or shipments through Asia, so higher tanker costs and premiums directly raise natural gas prices. Heating oil (diesel) in China/India will similarly rise, impacting manufacturers and farmers (e.g. higher transport or irrigation costs). For consumers in cold regions, any gas shortage could spike electricity bills. The overall economic impact is a small but notable inflationary pulse globally, layered atop already low growth.

China’s 2026 Strategy: Self-Reliance in Context

China’s leadership has taken note. Beijing’s 2026 budget and policy statements (presented early March) emphasize industrial self-reliance and resilience to external shocks. For example, China pledged record fiscal and R&D spending – including large outlays for semiconductors, AI and advanced manufacturing – to “cope with risks and market volatility”. High energy costs and disrupted shipping put a premium on domestic energy supply and supply-chain security. While China remains the world’s top oil importer (84% import-dependence), it has been diversifying (growing renewables, LNG infrastructure). In practice, China may accelerate alternative energy (like expanded LNG terminals, pipeline deals with Russia) and stockpile building. The 2026 plan’s focus on “new engines” (ICs, robots, low-altitude economy) suggests a push to produce more value added domestically, insulating from trade disruptions.

Trade flows will be affected: China has already rerouted some crude imports from the Gulf to West Africa and Latin America when prices fell during diversion. With higher freight costs, China’s crude importers may prefer shorter routes (e.g. via Russia, Central Asia, or reverse shipments). Analysts suggest Beijing will also lean on domestic stimulus (e.g. a $1tn infrastructure spending boost) to maintain demand while encouraging energy saving (e.g. power rationing if needed). In short, China’s response is to double down on resilience: using fiscal firepower to spur tech and infrastructure that reduce sensitivity to global oil shocks.

Shipping Insurance, Rerouting, and LNG Market Dynamics

The disruption forced major changes in logistics. Rerouting: With the Suez Canal/Bab el-Mandeb route unstable and Hormuz closed, many vessel operators are detouring via the Cape. This adds 10 14 days to Asia-Europe voyages, raising charter rates sharply. Maersk, MSC and CMA CGM explicitly suspended Gulf/Suez sailings. While safety increased, costs did too. These costs ultimately filter into fuel and goods prices; even transits from Atlantic producers (e.g. Nigeria, US) now require more ships.

Insurance: With war-risk coverage withdrawn, insurers or governments now face a choice. Some states (like India) might partially underwrite their tankers, but Western Europe is debating whether the EU should extend ACI mechanisms to maritime insurance (like it did for alternative fuels). Short-term, freight rates remain inflated – spot routes to Asia jumped ~4% in mid-week to W225, ~$12m per VLCC. LNG cargoes are also affected: tanker rates to Europe via Cape have nearly doubled, and rerouting Qatari LNG shipments around Africa will tighten global LNG supply and raise prices. China and Japan may not immediately see shortages (they have pipeline and LNG storage), but higher spot prices will come into play in the next quarter.

LNG Spot: Demand for alternative LNG has surged. Japan’s utilities, already over-contracted, likely face higher spot rates if Asian demand holds. Europe might seek extra LNG (with US Henry Hub also rising on higher oil linkage). The price of LNG in Asia jumped ~10–15% in early March as buyers scrambled, though some contracts are oil-indexed, muting long-run volatility. Overall, shipping risks add a premium to LNG and marine fuels globally.

EU Anti-Coercion and Policy Measures

The EU and other governments moved to cushion impacts. The EU’s Anti-Coercion Instrument (ACI) – originally designed to counter energy sanctions pressure – was cited by Spain when it declared non-application of US secondary sanctions to Spain-Iran oil trade. While the ACI is still being activated, Brussels hinted it could shield countries facing such coercion. On March 3, Spain invoked the ACI threat by passing a law (mirroring non-recognition of US secondary sanctions) to maintain Iranian oil swaps. This reassured markets that at least some supply corridors (to Iberia) might remain open, mitigating global price panic.

National strategic reserve releases are another tool. On Mar 4, the U.S. announced release of 30m barrels from the SPR (in coordination with allies) to calm markets. Some European countries (UK, Germany) also dipped into reserves or announced intent to do so if needed. These releases aim to cap near-term price spikes, though their effect is modest if the conflict drags on. Simultaneously, governments have signaled possible release of gas stocks into the spot market if LNG shipments are disrupted.

Trade resilience: Beyond emergency measures, policymakers discuss longer-term responses. The EU is reviewing its import diversification (e.g. securing more pipeline gas from Azerbaijan, North Africa, or LNG terminals). Investments in renewables and energy efficiency get a political boost as insurance against geopolitical risk. Asia’s central banks (India, China) stress that their inflation outlook remains steady, implying fiscal buffers or exchange rate shifts to absorb price jumps.

Scenarios and Recommendations

Scenario 1 – Rapid de-escalation: If diplomatic back-channels succeed (e.g. UN-brokered ceasefire or regional talks), shipping may resume in weeks. OPEC producers could ramp output back up. Oil might soften from the $85+ range, stabilizing around $70–80. Pass-through to consumers would be a short-lived shock, giving central banks space to stay accommodative. Governments should then focus on repairing insurance markets and gradually restocking reserves. Diplomatic engagement (e.g. EU-Iran talks, Gulf security talks) will be key to prevent recurrence.

Scenario 2 – Prolonged crisis: Continued strikes and counter-strikes could keep Hormuz shut for months. Oil could breach $100/bbl, and countries like Iraq or Kuwait might shut 3–5 mbpd permanently if storage is exceeded. Energy price inflation could reach 2–3% in Europe and North Asia, stalling growth. In that case, sharp demand restraint (e.g. EU urging lower speed limits, delayed heating) and large SPR releases become essential. International collaboration on shipping (e.g. convoys, insurance pools) would be needed. The ACI or similar tools might be expanded to explicitly protect trade routes and energy contracts. The risk of economic retaliation by Iran or US sanctions would complicate responses.